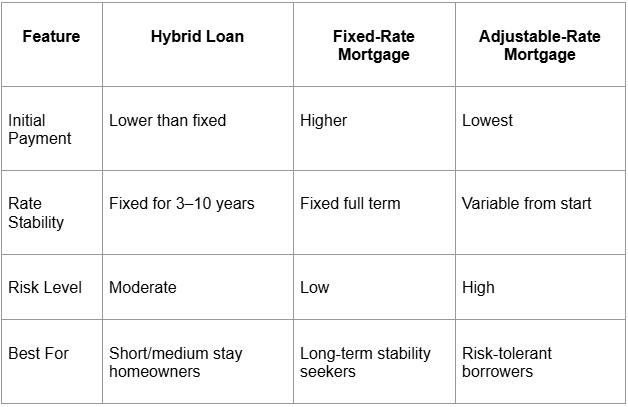

A hybrid loan is a mixture of two types of loans—specifically a fixed-rate loan and an adjustable-rate mortgage. The term hybrid in hybrid-loan refers to the fixed period of the loan, usually between two and five years.

You'll find hybrid loans in several configurations: 3/1, 5/1, 7/1, and 10/1 structures. The 3/1 ARM keeps your rate locked for three years, then adjusts every year after that. Most lenders price these loans about 0.25% to 0.75% below similar fixed-rate mortgages, which creates immediate savings.

A hybrid is different than an interest-only loan because it applies more money toward the principal of the loan. This results in more cash flow and a higher level of equity.

Related: What Exactly is a Purchase Money Loan

Hybrid loans begin at a lower rate than the standard 30-year fixed-rate mortgage. This offers some protection if the interest rates rise dramatically.

That rate difference translates to real money. On a $300,000 loan, even a 0.5% gap between hybrid and fixed rates saves you roughly $150 each month during the initial period. It might not sound like much, but you're looking at substantial savings over multiple years when you add it all up.

Consider choosing between a 30-year fixed loan at 6.5% and a 5/1 hybrid ARM at 6.0%. On a $350,000 mortgage, the fixed loan runs about $2,212 monthly while the hybrid costs closer to $2,098 during the fixed period. That $114 monthly difference adds up to nearly $7,000 in savings over the first five years, which explains why many buyers gravitate toward hybrid structures when managing early homeownership costs.

These hybrid loans utilize a fixed rate for a period of three, five, seven, or ten years. During that time, payments and rates will stay the same. When the loans are listed, the first number tells you how many years the rate is fixed. For example, a 3/1 hybrid mortgage holds the same rate for the first three years.

Think of the fixed period as your financial runway. You can plan your budget without worrying about payment surprises because your housing cost stays predictable. This stability works especially well for first-time buyers or anyone expecting their income to grow during those early years.

Buyers with predictable career trajectories often use the fixed period as a financial launch pad. A teacher, nurse, or engineer expecting steady raises can plan to refinance or absorb payment increases down the road. Someone with unpredictable income might struggle if the adjustment period arrives during financial instability. Mapping out your income trajectory matters just as much as crunching rate numbers.

Once the fixed period of the loan ends, the interest rate can change. The second number in the loan terms tells you how often the rate can adjust thereafter. For example, in a 3/1 loan, the rate can adjust annually after the initial three years.

Rate changes follow specific benchmark indexes, typically the Secured Overnight Financing Rate (SOFR). Your lender tacks on a margin, usually between 2% and 3%, to whatever the current index shows. Most hybrid loans come with caps that prevent your rate from jumping too dramatically during each adjustment period, which protects you from extreme swings.

Adjustment math gets confusing quickly. If the SOFR index hits 4.5% and your loan margin is 2.25%, your new rate becomes 6.75%, unless caps prevent the full jump in one year. Most lenders use "look-back periods," averaging index values from the past 30 to 45 days to calculate changes. That buffer prevents rates from swinging wildly with daily market movements.

Your monthly payment will change as interest rates change. These payments are calculated to help you pay off your debt and any extra interest that accrues over time. Higher rates result in higher payments—while lower rates can reduce your payment amount.

Payment shock is your biggest concern with hybrid loans. Smart borrowers run worst-case scenarios before signing anything, making sure they can handle potential payment jumps if rates climb significantly. You don't want to be caught off guard when the adjustment period hits.

Related: Questions to Ask a Mortgage Lender

Lower starting rates are enticing, but they do come with risk. Hybrid loans make the most sense under the right circumstances.

Before choosing a hybrid loan, take an honest look at your finances and housing timeline. These loans reward strategic thinking but can backfire on borrowers who don't grasp the adjustment risks. You need to understand what you're getting into.

Hybrid loans also attract younger buyers expecting major life changes. Starting a family, relocating for work, or planning graduate school are common reasons to choose a loan that minimizes upfront costs. These borrowers prioritize flexibility and short-term affordability over long-term rate security, betting on their ability to adapt when adjustments kick in.

If you plan to refinance or move within a short period, a hybrid loan can be a great fit. It allows you to benefit from the lower rate and potentially pay off the loan before adjustments begin. However, if your plans change, you may end up paying more in the long run.

Military families and corporate employees who expect transfers often use hybrid loans strategically. They capture the rate savings during their expected ownership window without stressing about future adjustments they won't be around for. It's a calculated move that makes sense for their situation.

One way to reduce the risk of future rate hikes is to make additional payments toward your principal. This helps pay off the loan faster—before rate changes occur.

Even an extra $100 monthly can chip away at your loan balance significantly and reduce the sting of future rate increases. Some borrowers automatically funnel their initial payment savings into additional principal payments, which builds equity faster.

While interest rates can rise, they can also fall. If rates drop, it may benefit you with lower payments. However, interest caps may limit how low your rate can go protecting you from spikes, but also from fully benefiting from decreases. Learn more about interest rates.

Lower early rates can help improve your credit score with consistent, on-time payments. But once rates adjust, your ability to requalify for new loans at favorable terms may be limited if your credit hasn't improved enough.

Hybrid loans can work well for borrowers whose credit scores fall just below prime lending thresholds. The lower initial payments give you breathing room for debt reduction and credit repair activities, potentially improving your overall financial picture.

Related: 580 Credit Score Home Loans

Two main factors influence your rate: the lender’s index rate and the spread they add. These are affected by rate caps:

As with any loan, hybrid loans have both pros and cons. They combine fixed and variable rate structures, offering both flexibility and uncertainty.

Lower initial payments often help borrowers qualify for larger loan amounts or meet debt-to-income requirements that might otherwise block them. Unlike fixed-rate mortgages, hybrid loans automatically capture benefits when rates fall without forcing you through expensive refinancing costs.

Many financial experts appreciate the balance of combining fixed and variable rates. Lenders often market hybrid loans as a balanced approach, offering two types of stability within a single loan structure.

While the concept seems simple, hybrid loans can be confusing in practice. If you prefer a straightforward, predictable loan structure, hybrid loans might feel overwhelming or too volatile.

Hybrid loans demand more financial knowledge than traditional mortgages. You need to understand indexes, margins, caps, and adjustment mechanics to make informed decisions. Poor timing can leave you paying more than conventional alternatives would have cost.

Unlike variable rates, a fixed-rate portion won’t adjust downward if the market improves. That means if rates fall, you’re locked into the higher rate, which is the “gamble” with hybrid loans.

This opportunity cost represents money you could potentially save with different loan structures. The fixed period does protect against rate increases though, making it a calculated trade-off rather than a pure disadvantage. You're weighing short-term savings against long-term uncertainty.

Lenders typically qualify you based on the fully-adjusted payment rather than just the teaser rate. This approach confirms you can afford the loan even if rates climb to maximum levels. Most hybrid loans require 10% to 20% down payments, similar to conventional mortgages.

Understanding complex scenarios like purchase money loan transactions or deals subject to an existing loan can provide additional context where hybrid loans might play a strategic role.

For more detailed information about specific structures, resources like what is a hybrid mortgage and hybrid mortgage loan guides offer additional perspectives.

Getting the best deal on a hybrid loan is all about timing—but it’s possible. These loans can offer a secure option during times of changing interest rates. Understanding your options before committing can set you up for long-term success.

Want to work with a Certified Mortgage Planning Specialist? Mares Mortgage is a proud member of the National Association of Mortgage Professionals and can help you find the perfect loan for your needs.

.png)